Australian shorn wool production estimate of 318 Mkg greasy in 2023/24 and forecast 285 Mkg greasy for 2024/25

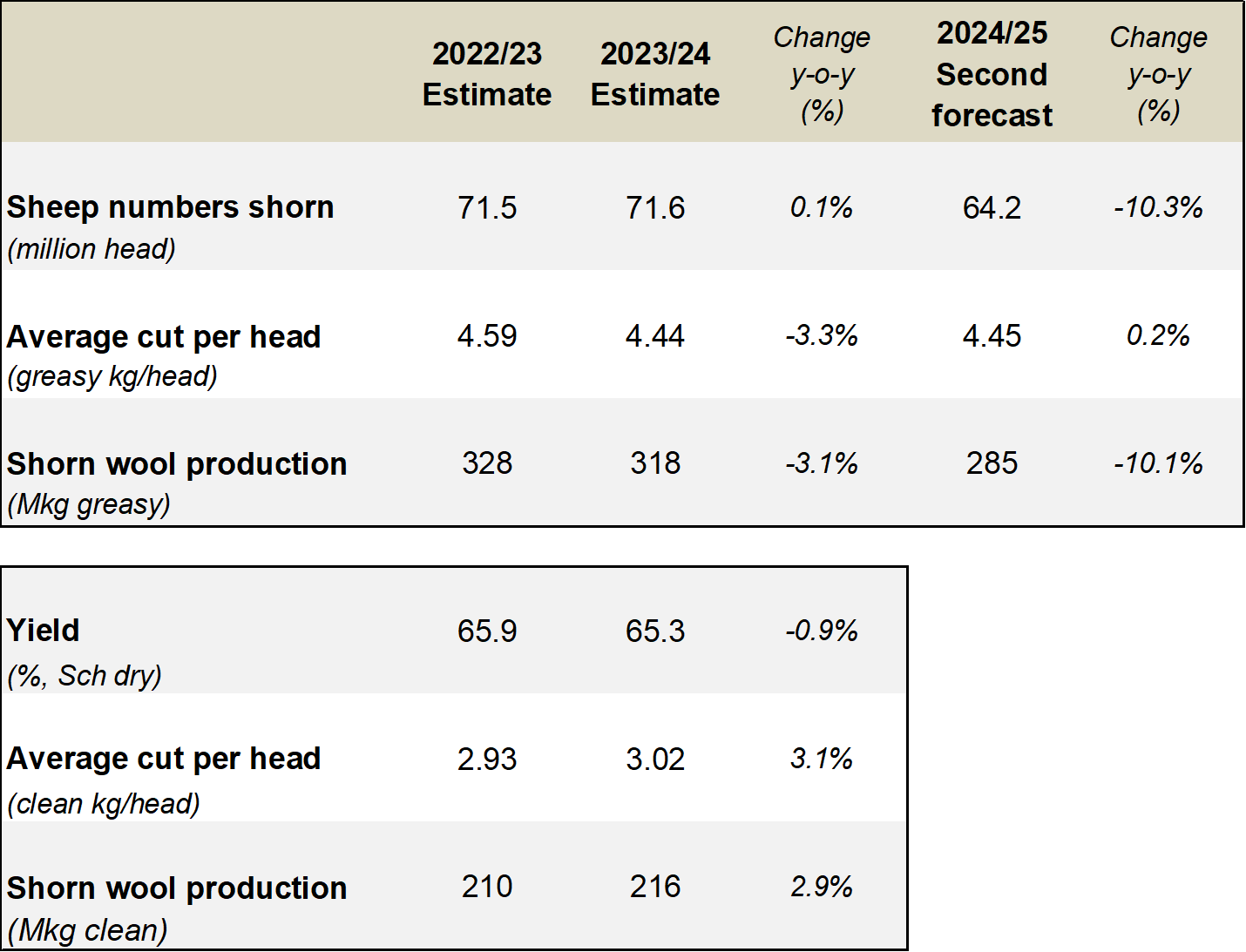

The Australian Wool Production Forecasting Committee’s (AWPFC) estimate of shorn wool production for the 2023/24 season is 318 million kilograms (Mkg) greasy. This is 3.1% lower than the 2022/23 estimate and a 6 Mkg greasy downward revision of the April forecast.

- The Australian Wool Production Forecasting Committee’s estimate of shorn wool production for 2023/24 is 318 Mkg greasy, 3.1% lower than the 2022/23 season estimate. The number of sheep shorn is estimated at 71.6 million head, up 0.1%. However average cut per head is estimated to have reduced to 4.44 kg greasy (down 3.3%) due to poorer season.

- The AWPFC’s second forecast of shorn wool production for the 2024/25 season is 285 Mkg greasy, a 10.1% decrease on the 2023/24 forecast. The number of sheep shorn is forecast at 64.2 million, down 10.3%. Average cut per head is expected to be comparable with 2023/24 at 4.45 kg greasy.

Committee Chairman, Stephen Hill said that "the deterioration in seasonal conditions in western Victoria, South Australia, Western Australia, Tasmania and southwest New South Wales since the April meeting prompted the downward revision of the April forecast”. Held over lambs and older breeding ewes that were retained in the flock at the beginning of the season have now been turned off prompted by the recovery of sheepmeat prices in recent months.

“Sheep shorn numbers were comparable to the 2022/23 season at 71.6 million head, up 0.1%. However, the relatively poorer seasonal conditions in 2023/24 reduced average cut per head to 4.44 kg greasy, down 3.3%. This is close to the long-term average following historically high per head production in 2022/23”.

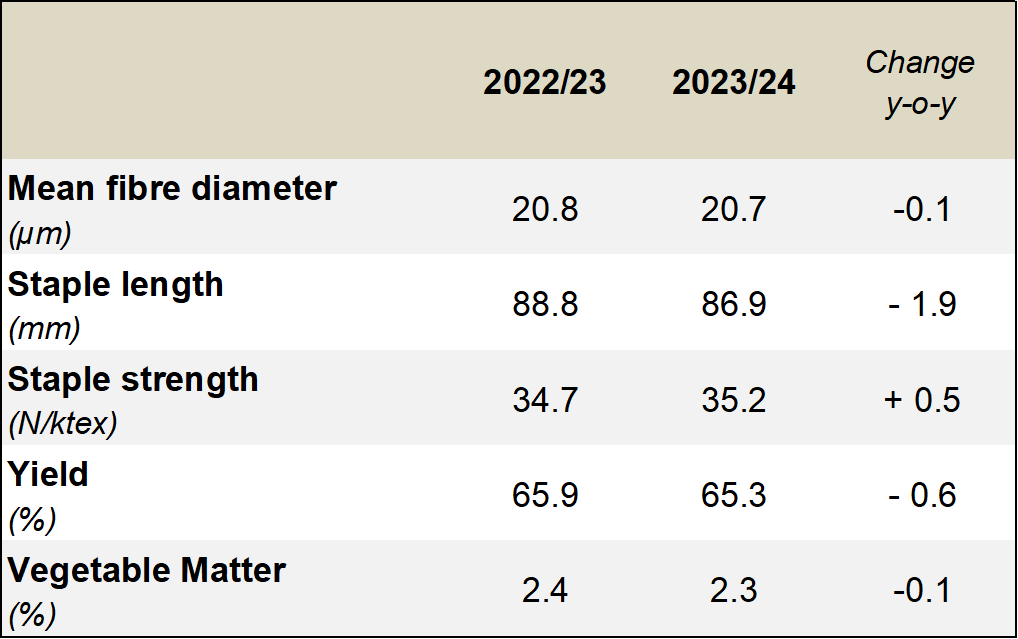

AWTA key test data for the 2023/24 season show a 0.1 micron decrease in mean fibre diameter to 20.7 microns, a 1.9 mm decrease in staple length to 86.9 mm, 0.6% lower yield to 65.3% and 0.1% less VM (2.3%). Staple strength increased to 35.2N/ktex (up 0.5 N/ktex). The weighted average fibre diameter of firsthand Merino wool auctioned in 2023/24 was 18.8 microns (down 0.2 microns on the 2022/23 season).

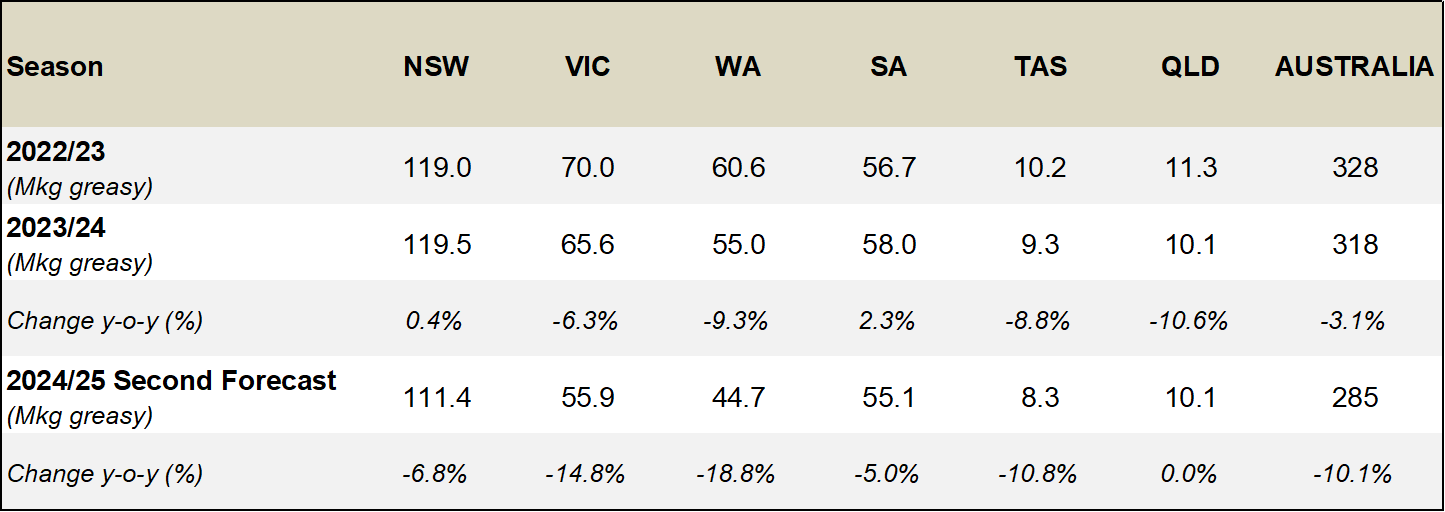

New South Wales continues to have the largest sheep flock, shearing 26.6 million head (up 2.7%) and producing 119.5 Mkg greasy wool (up 0.4%). Victoria shore 15.6 million sheep (down 3.1%) and produced 65.6 Mkg greasy (down 6.3%) with Western Australia producing 55.0 Mkg greasy (down 9.3%) from 12.5 million sheep shorn (down 4.2%).

AWTA wool test volume for the 2023/24 season (334.5 Mkg greasy) was down by 3.8% on a year-on-year basis. Firsthand offered wool at auction during 2023/24 was not different to the amount offered in 2022/23 at 298 Mkg greasy.

The August AWPFC estimate includes a clean wool estimate for average cut per head and shorn wool production. For the 2023/24 season the yield (%, Schlumberger dry top and noil yield) from the AWTA key test data was used to calculate the clean average cut per head and clean shorn wool production (Table 1).

Poor seasonal conditions in western Victoria, Tasmania, South Australia and Western Australia have prompted the AWPFC to revise its second forecast of shorn wool production for the 2024/25 season down to 285 Mkg greasy, a 10.1% decrease on the 2023/24 estimate. The May 2024 Sheep Producer Intentions Survey (SPIS) indicated a reduction in producer sentiment regarding both the wool and sheepmeat sectors compared to sentiment in May 2023. Seasonal conditions, feed availability, input costs, availability of labour as well as sheep and wool prices are the key factors impacting on-farm decision making.

The Bureau of Meteorology is forecasting average to above average median rainfall in Queensland, New South Wales, Victoria and Tasmania from September to November, but below average rainfall is expected in South Australia and Western Australia. Producers in most states will reassess their stocking rate if feed availability remains limiting in spring. On-farm stock water availability leading into summer is another key consideration.

The AWPFC will review its 2024/25 forecast in December when the seasonal and market outlook becomes clearer.

Table 1: Summary of Australian wool production

Note: Totals may not add due to rounding.

Table 2: Total shorn wool production by state

Note: Totals may not add due to rounding.

Table 3: AWTA key test data for 2022/23 and 2023/24

The National Committee drew on advice from the six State Committees, each of which includes growers, brokers, private treaty merchants, sheep pregnancy scanners, representatives from State Departments of Agriculture and the Australian Wool Testing Authority. Data and input were also drawn from AWEX, wool exporters, the Australian Bureau of Statistics, ABARES, and Meat and Livestock Australia.

The state and national Committees will next meet in mid-December 2024.

The full forecast report will be available on the AWI website at www.wool.com/forecasts from 23rd August 2024.

Released by:

Kevin Wilde

Australian Wool Innovation, General Manager, Consultation and Engagement

Mobile: +61 436 031 277